Forced to rebuild from scratch, the Mumbai-based couple, now in their early 50s, navigated corporate comebacks and personal sacrifices to stand as a testament to the power of perseverance and being financially savvy. Today, they believe that true wealth lies not just in earning, but in managing what you have.

Early life

With a shared passion for making a difference, Unny and Bindhu embarked on their careers. In 1997, Unny joined a corporate firm committed to social impact, drawn by its mission to change the world.

Unny describes this period as transformative, aiding his personal growth. However, the company faced significant difficulties, resulting in unpaid salaries for almost two years, leading to his personal bankruptcy.

“From 1997 to 2003, I worked for a company dedicated to making a significant social impact. We operated on modest salaries, aligning with the company’s mission to make a difference.”

“However, towards the end, it came to a grinding halt with no salaries for two years. But being in our early 30s, we were thinking about changing the world and we just continued, till it became a livelihood issue,” Unny recalled.

Bindhu, determined to support the family, took up work as a features writer.

Fortunately, Unny’s background in marketing and early experience as a programmer helped him secure a senior position at one of India’s first digital marketing agencies in 2003.

According to Unny, this role was pivotal in restarting their lives, with advance payments from the company allowing them to clear household bills and cover rent, bringing the much-needed relief.

At this point in time, their first priority was to achieve financial stability. To ensure his finances were in order, even if he decided to return to unconventional career options, Unny sought guidance from a financial advisor. Subsequently, in 2011, he approached Ladder7 Wealth Planners, recommended by a colleague.

Portfolio mix

Initially, neither Unny nor Bindhu had any experience with investing or financial planning. They primarily parked their savings in bank accounts, and occasionally purchased mutual funds with minimal understanding of how it would impact their finances in the long run.

View Full Image

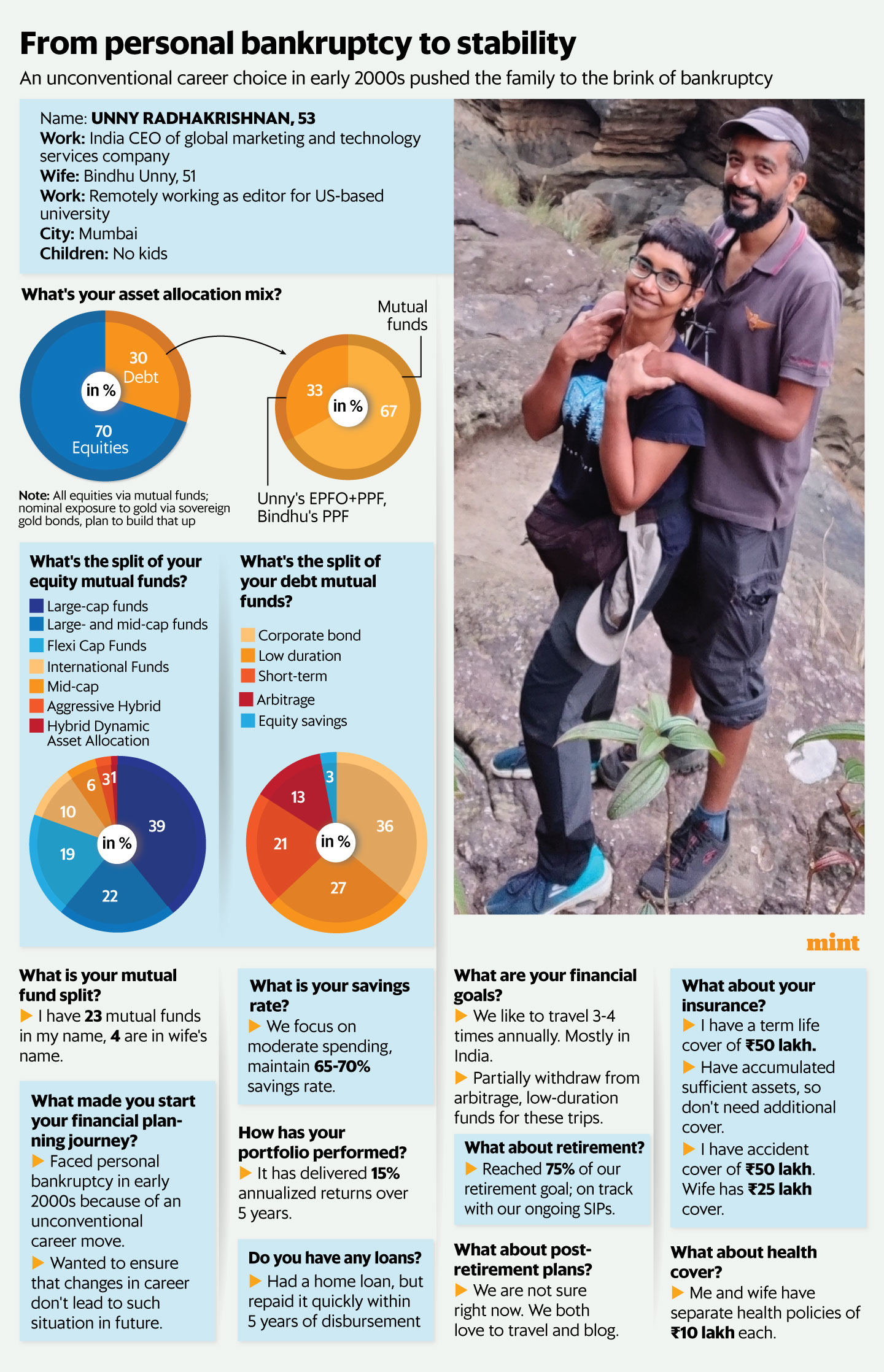

Nearly 70% of their investments are in equity, and the rest primarily in debt.

Cut to 2024, the couple has built a diversified investment portfolio with a balanced mix of equity and debt. Nearly 70% of their investments are in equity, and the rest primarily in debt.

Nearly 40% of the equity mutual funds are allocated to large-cap funds, around 20% to large- and mid-cap funds, and another 20% to flexi-cap funds. About 10% is invested in international funds, with the remaining equity exposure spread across various fund categories.

Over the past five years, their portfolio has delivered annualized returns of 15%.

The debt portfolio includes 20% in debt mutual funds, 10% in Unny’s employees’ provident fund account, and public provident fund (PPF) investments for both Unny and Bindhu.

Of the debt mutual funds, 36% is allocated to corporate bond funds, 27% to low-duration funds, 20% to short-term funds, 12% to arbitrage funds, and about 3% to equity savings funds.

Bindhu works remotely as a developmental editor for a US-based university on a contractual basis. Since she does not enjoy the benefits of an employer provident fund, she fills the gap by investing in PPF.

The couple has also started investing in sovereign gold bonds (SGBs), albeit with nominal holdings, but plans to gradually increase this exposure. Unny has 23 mutual funds in his name, while Bindhu has four.

Financial goals

In 2018, Unny took a break from his corporate career to re-enter the social sector as planned. “I consulted my advisor about making the switch, and he said I was in a position to do it, even with a reduced salary,” Unny said.

However, in 2020, he returned to corporate life, seizing the opportunity to join as the chief executive officer of a global marketing and technology services company’s Indian operations.

Both Unny and Bindhu enjoy traveling and blogging about their experiences. “We take three to four trips annually,” he said. They cover travel expenses by withdrawing from arbitrage and low-duration funds as required.

Early in their lives, the couple had decided not to have children, so they do not need to plan for education or wedding-related expenses.

The couple is well on their way to reaching their retirement corpus, having achieved 75% of their target. They have not yet made any specific plans for retirement, but both Unny and Bindhu are passionate about travel and writing, and are certain they will continue to pursue these hobbies after retiring.

Spending habits

The couple maintains a high savings rate of 65-70% and has no outstanding loans. According to Unny, experiencing a financial crisis early in their lives taught them to be moderate in their spending habits. “We repaid our home loan within five years.”

“Our belief is that getting wealth is not just about earning it, but it is also about how you manage it,” Unny added.

Insurance

Unny has a term life insurance policy of ₹50 lakh. He said now they have accumulated enough assets, and do not need additional coverage.

Both Unny and Bindhu have separate health insurance policies of ₹10 lakh each. Unny also has personal accident coverage of ₹50 lakh, while Bindhu has a ₹25 lakh accident coverage policy.

Images are for reference only.Images and contents gathered automatic from google or 3rd party sources.All rights on the images and contents are with their legal original owners.

Comments are closed, but trackbacks and pingbacks are open.